How to Lower Your Car Insurance Rates

25+ Years of Trusted Service *

Call us 1-855-620-9443

25+ Years of Trusted Service *

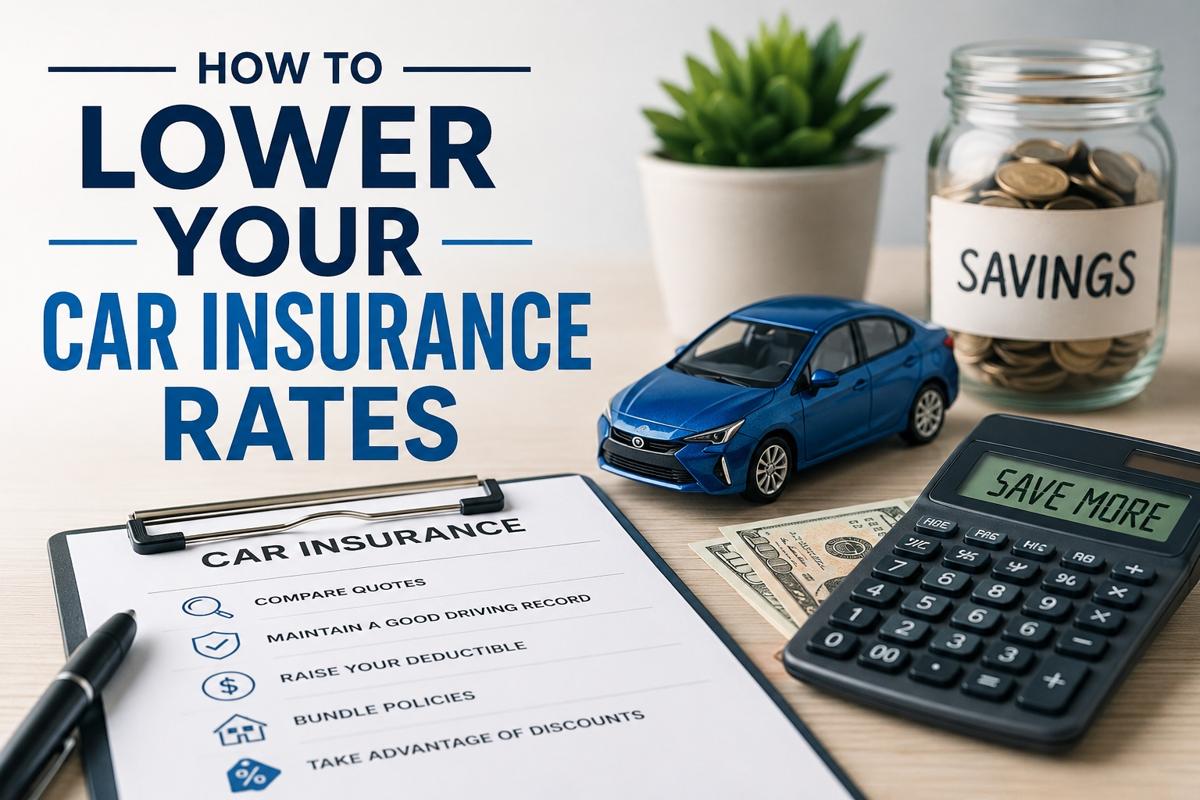

Looking for ways to lower your car insurance rates? Getting cheaper auto insurance may be easier than you think. By comparing quotes, reviewing your coverage, asking about discounts, and making smart policy changes, you may be able to reduce your premium without sacrificing the protection you need.

At Young America Insurance, you can compare multiple car insurance quotes online or over the phone in just minutes. Here are practical ways to reduce your auto insurance costs and keep more money in your pocket.

Your auto insurance policy may include coverage options you no longer use. Before removing anything, review your current auto insurance coverage options so you understand what each part of your policy does and what you may still need. Reviewing your policy can help you identify extras that may be increasing your premium.

Consider reviewing these common add-ons:

Before making changes, review your updated premium and policy declarations to confirm your savings.

Safe driving is one of the best ways to lower car insurance rates. Drivers with fewer accidents, tickets, and violations often qualify for better rates.

To help keep your premium low:

Avoid speeding tickets and traffic violations that may increase your car insurance rates.

Drive defensively to reduce your risk of accidents, claims, and future premium increases.

Never drive under the influence, since a DUI can significantly raise your insurance costs.

Ask whether traffic school can help keep a ticket off your record and protect your rate.

A DUI or major violation can significantly increase your insurance costs, especially for younger drivers. If you need affordable options, compare younger drivers insurance coverage to find a policy that fits your needs and budget.

In many states, a strong credit score can help you secure lower auto insurance premiums. Check your credit report regularly for accuracy. Dispute and fix any errors to boost your score over time. Good credit will help you get cheaper car insurance and reduce financing costs for big-ticket items, like a new car or home. However, some providers also offer car insurance options for drivers with no credit check, which may be helpful in certain cases.

Many of the best insurance deals are found online. Insurance websites like Young America Insurance make it easy to compare rates from dozens of providers in just minutes. Most consumers save up to $600 by switching. You can get a quote in minutes using just your smartphone.

Another way to lower your car insurance rates is to choose a higher deductible. Your deductible is the amount you pay out of pocket before your insurance coverage helps pay for a covered claim. In many cases, increasing your deductible can reduce your monthly premium.

Important

Before raising your deductible, make sure you have enough savings to cover the higher out-of-pocket cost if you need to file a claim.

For example, raising your deductible from $500 to $1,000 may help lower your insurance costs. This is one strategy often mentioned when looking for dirt cheap car insurance, but it only makes sense if you can comfortably afford the higher out-of-pocket expense after an accident. Before making this change, compare the monthly savings with the amount you would need to pay if you file a claim.

Car insurance discounts can make a big difference in your final premium. Many drivers qualify for savings but do not always know which discounts are available. When comparing quotes, ask each insurance company which discounts may apply to your situation.

Common auto insurance discounts may include:

Even small discounts can add up over time. If your personal situation has changed recently, such as moving, getting married, improving your driving record, or driving fewer miles, you may be eligible for new savings. You can also compare affordable car insurance quotes to see which providers offer the best discounts for your profile.

Bundling your auto insurance with another policy may help you get a lower rate. Many insurance companies offer discounts when you buy more than one type of coverage from the same provider.

For example, you may be able to bundle car insurance with renters insurance, homeowners insurance, motorcycle insurance, or another eligible policy. Some drivers looking for flexible payment options also compare buy now pay later car insurance plans while checking whether bundling can lower their total cost.

Before bundling, compare the total cost of both policies. A bundle discount is helpful only if the combined price is still lower than buying separate policies from different companies.

The type of vehicle you drive can affect how much you pay for car insurance. Some cars cost more to insure because they are expensive to repair, have higher theft rates, include costly parts, or are more likely to be involved in claims.

Before buying a new or used car, it is a good idea to compare insurance quotes for that vehicle. A car with strong safety features, affordable repair costs, and a lower claims history may help you qualify for cheaper auto insurance.

If lowering your monthly costs is a priority, avoid choosing a vehicle based only on the purchase price. The long-term cost of insurance, maintenance, fuel, and repairs should also be part of your decision.

Car insurance rates can change over time, even if your driving habits stay the same. That is why it is smart to review your policy every 6 to 12 months. If your current premium is too high, you may want to switch car insurance companies after comparing quotes and confirming that the new policy gives you the coverage you need.

You should also review your policy after major life changes, such as moving to a new ZIP code, buying a different car, getting married, adding or removing a driver, or improving your credit score. These changes may affect your premium and could help you qualify for a lower rate.

Taking a few minutes to review your policy can help you avoid overpaying for coverage you no longer need. It can also help you make sure you still have the right protection for your vehicle, budget, and driving habits.

A new ZIP code can affect your insurance rate.

Different vehicles can cost more or less to insure.

Adding or removing a driver may change your premium.

Compare quotes before your current policy renews.

Now that you know how to lower your car insurance rates, the next step is to compare your options. Review your current coverage, ask about discounts, and get quotes from multiple providers. With the right strategy, you may be able to reduce your premium while keeping the protection you need on the road.