Getting car insurance under $100 a month is possible, but it requires smart decisions about coverage, vehicle choice, driving behavior, and insurer selection. While many drivers assume ultra-cheap insurance is unrealistic, the truth is that millions of Americans can qualify for sub-$100 monthly auto insurance – especially when they understand how insurers calculate risk.

Auto insurance pricing is complex. Rates are influenced by dozens of variables, many of which are outside your direct control, such as age, marital status, ZIP code, and insurance history. Others, however, are entirely within your control. By optimizing those factors, you can dramatically increase your chances of staying under the $100-per-month threshold.

This guide explains exactly how low-cost car insurance works, who qualifies, which insurers consistently offer the cheapest rates, and how different age groups—teens, adults, and seniors—can realistically reach that price point.

Why $100 a Month Is a Realistic Benchmark

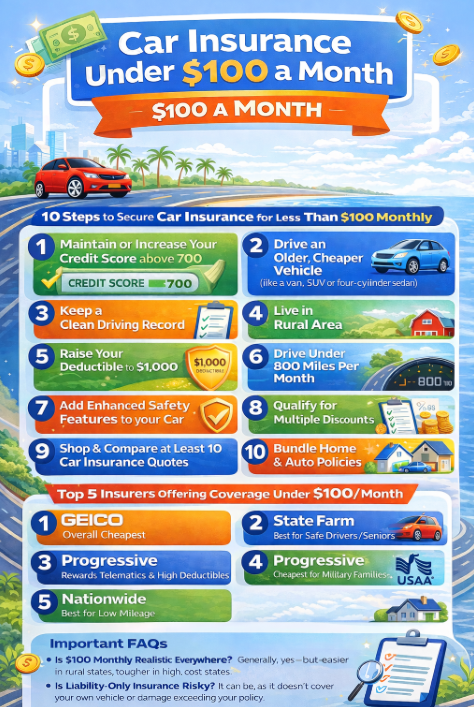

A $100 monthly premium equals $1,200 per year. For insurers, this price point usually aligns with drivers who present low financial risk. That typically means fewer claims, lower repair costs, and predictable driving patterns.

Drivers most likely to qualify include:

- Those with clean driving records

- Owners of older or inexpensive vehicles

- Low-mileage drivers

- People with strong credit

- Drivers who select higher deductibles

- Policyholders who qualify for multiple discounts

Liability-only policies are the most common way to stay under $100, but some drivers can even maintain full coverage at that price with the right setup.

How Insurers Calculate Monthly Car Insurance Rates

Insurance companies rely on actuarial models that predict how likely you are to file a claim and how expensive that claim might be. The most influential pricing factors include:

Driving Record

A clean record with no tickets or at-fault accidents is the single biggest factor in achieving ultra-low rates.

Vehicle Type

Four-door sedans, older SUVs, and vehicles with four-cylinder engines are cheaper to insure than sports cars, luxury models, or high-performance vehicles.

Mileage

Driving fewer than 800 miles per month significantly reduces risk exposure and unlocks low-mileage discounts.

Credit Score

In most states, drivers with credit scores above 700 pay substantially less than those with poor credit.

Coverage Level

Liability-only coverage is dramatically cheaper than full coverage, especially for older vehicles.

Deductible

Raising your deductible to $1,000 or more can shave $20–$40 off monthly premiums.

Top 5 Car Insurance Companies Offering Coverage Under $100 a Month

While rates vary by state and driver profile, certain insurers consistently rank among the cheapest for qualifying drivers.

Liability Car Insurance for $50 or Less Per Month

Liability insurance is mandatory in nearly every state. These policies cover damage and injuries you cause to others, but do not protect your own vehicle.

Drivers who often qualify for liability insurance under $50 per month include:

- Retirees

- Unemployed individuals

- Students with limited driving

- Drivers with older vehicles

- Rural residents

The biggest risk of minimum liability insurance is underinsurance. A single accident involving a newer vehicle or medical claims can quickly exceed state minimum limits.

Should You Buy Higher Liability Limits?

While minimum coverage keeps costs low, it can expose you to lawsuits and financial loss. A common recommendation among insurance professionals is the 100/300 rule, meaning:

- $100,000 bodily injury per person

- $300,000 bodily injury per accident

Drivers with assets exceeding $100,000 should strongly consider higher limits, even if it pushes premiums slightly above $100 per month.

Can Teens Get Car Insurance Under $100 a Month?

Teen drivers are statistically the riskiest drivers on the road. As a result, standalone policies for teens almost always exceed $100 per month. However, it is sometimes possible under specific conditions. The most effective strategies include:

Even with all discounts, under-$100 teen insurance is rare but not impossible.

Senior Car Insurance Under $100 a Month

Seniors are among the cheapest drivers to insure. Lower mileage, decades of experience, and safer driving habits work heavily in their favor.

Most seniors can easily qualify for:

- $60–$90 monthly liability coverage

- Even lower rates with low mileage

- Discounts for defensive driving courses

Removing collision and comprehensive coverage on vehicles worth under $5,000 often brings premiums well below $100.

Why Older Cars Are Cheaper to Insure

Vehicle value plays a massive role in pricing. Older vehicles cost less to repair or replace, reducing insurer risk.

Cars that are:

- 5–10 years old

- Four-door

- Four-cylinder

- Non-luxury brands

Used SUVs and sedans like the Toyota Camry or Honda Accord often produce the lowest premiums.

Can You Get Full Coverage Under $100 a Month?

It’s difficult but not impossible.

Drivers who manage it typically:

- Own older vehicles

- Have strong credit

- Raise deductibles to $1,000 or more

- Drive under 800 miles per month

- Qualify for multiple discounts

Leased or financed vehicles almost always require comprehensive and collision coverage, making under-$100 premiums less likely.

The Role of Credit Score in Cheap Car Insurance

In most states, a credit score is one of the strongest predictors of insurance cost. Drivers with scores above 700 are statistically less likely to file claims.

Improving your credit score can reduce premiums by 30–50% over time.

Discounts That Can Push You Below $100

Many drivers miss discounts simply because they don’t ask. Common discounts include:

- Safe driver

- Low mileage

- Good student

- Senior

- Military or veteran

- Teacher

- Automatic payments

- Garaged vehicle

- Multi-policy bundling

Stacking just two or three discounts can be the difference between $130 and $95 per month.

Why Shopping Online Saves Money

Direct insurers operate with lower overhead, passing savings to customers. Comparing multiple quotes online takes minutes and often produces immediate savings.

Drivers who compare at least 10 quotes consistently find lower rates than those who only check one or two providers.

Frequently Asked Questions

Is car insurance under $100 a month realistic in every state? +

Is liability-only insurance risky? +

Can I lower my rate mid-policy? +

Does mileage really matter? +

What’s the single best way to lower my rate fast? +

The Final Word On Car Insurance Under $100 a Month

Car insurance under $100 a month is not a myth; it’s a strategy. By choosing the right vehicle, coverage level, insurer, and discounts, many drivers can stay well below that benchmark without sacrificing financial protection.

The key is understanding how insurers think and positioning yourself as a low-risk driver. With careful planning and comparison shopping, cheap car insurance is absolutely within reach. Compare the cheapest car insurance quotes online and save hundreds with direct rates.