Finding car insurance with no money down can feel overwhelming, especially when money is tight and coverage is needed immediately. Many drivers believe auto insurance always requires a large upfront payment, but that is not always the case.

The truth is, truly free car insurance does not exist. There are legitimate ways to get insured with little to no upfront cost, including zero-deposit billing and low down payment plans that can start as low as $20 in select situations.

This comprehensive guide explains how no money down car insurance works, who qualifies, how insurers determine deposits, and how to avoid common mistakes that make “cheap” insurance far more expensive over time.

What No Money Down Car Insurance Really Means

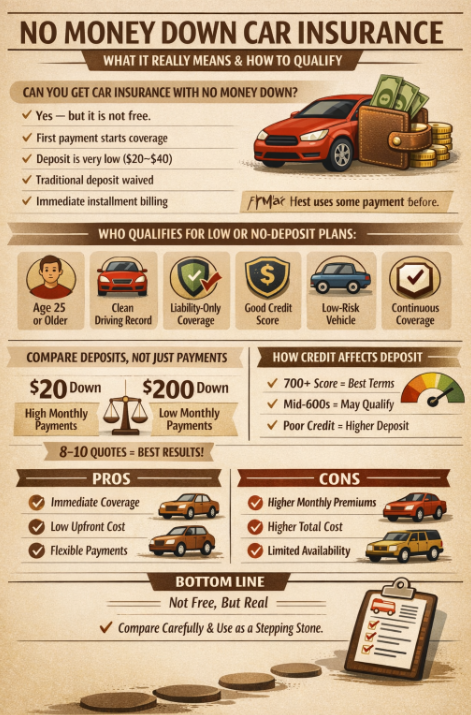

No money down car insurance does not mean you receive coverage without paying anything. Instead, it usually means one of the following:

Your first monthly payment acts as the initial payment

- The insurer waives a traditional deposit

- The required down payment is very low, often between $20 and $40

- The policy begins immediately under installment billing

Most insurance companies still require some form of payment before coverage starts. Even in states where zero-deposit insurance structures are allowed, insurers will not assume financial risk without receiving payment. In no-deposit arrangements, the first month’s premium effectively replaces a traditional deposit.

Understanding this distinction helps avoid confusion and prevents unrealistic expectations when shopping for coverage.

Why No Money Down Car Insurance Exists

Insurance companies offer low or no-deposit plans to remain competitive and reach drivers who might otherwise remain uninsured. From the insurer’s perspective, allowing installment billing expands their customer base, especially among younger drivers, seniors on fixed incomes, or individuals recovering from temporary financial hardship.

However, these plans come with trade-offs. Insurers typically charge higher monthly premiums to offset the increased risk of cancellation or missed payments. This is why no money down insurance should be viewed as a financial access tool, not necessarily the cheapest long-term option.

Tips to Qualify For No Money Down Car Insurance

Not all drivers qualify for no-deposit or $20 down insurance plans. Insurers reserve these options for applicants who present lower overall risk. Your chances improve significantly if you:

Maintain a clean or mostly clean driving record

- Are age 25 or older

- Choose liability-only coverage

- Avoid gaps in insurance history

- Have fair to good credit

- Drive a low-risk vehicle

- Maintain stable personal information

Drivers with DUIs, SR-22 filings, reckless driving convictions, or multiple recent accidents typically face higher deposit requirements or limited eligibility.

Common Myths About No Money Down Insurance

Many drivers are misled by advertising claims that oversimplify how low-deposit insurance works. No down payment insurance does not mean free insurance, nor does it mean the policy is illegal or intended only for high-risk drivers. In reality, many responsible drivers choose low-deposit plans for cash-flow management, not because they are risky to insure.

Another common misconception is that no-deposit insurance is always cheaper. While it lowers upfront costs, it often increases total annual premiums. Understanding this trade-off is essential.

When No-Deposit Insurance May Not Be the Best Choice

No-deposit insurance is helpful during financial hardship, but it is not always the most cost-effective long-term option. Higher monthly premiums often result in a higher total annual cost.

Drivers who can afford a deposit or prepaid premium often save hundreds of dollars per year. No-deposit insurance works best as a short-term solution, not a permanent strategy.

Why Comparing Down Payment Plans Matters

Comparing insurance quotes is not just about finding the lowest monthly payment. The required upfront deposit can vary dramatically between insurers.

One insurer may require $20 down with higher monthly premiums. Another may require $200 down but charge significantly less per month. Depending on your financial situation, either option could be the better choice.

Online comparison tools allow you to filter quotes by deposit size, monthly payment, coverage level, deductibles, and billing structure. Comparing at least eight to ten quotes dramatically improves your chances of finding the most affordable option.

Instant Auto Insurance With Low or No Deposit

Many insurers offer instant coverage once payment is submitted. Drivers can apply from a smartphone, receive proof of insurance immediately, and begin coverage the same day.

Monthly installment plans are the most common structure for no-deposit insurance. While these plans help manage cash flow, they often increase the total cost of coverage. Automatic payments are strongly recommended to prevent missed payments and policy cancellations.

Why Free Auto Insurance Does Not Exist

Some advertisements promise free or zero-cost auto insurance. These claims are misleading. Insurance companies cannot provide coverage without payment. Even zero-deposit policies require at least one premium payment before coverage becomes active.

The idea of “free insurance” persists because installment billing disguises the initial cost, but payment is always required.

Eligibility Requirements for No Money Down Auto Insurance

Eligibility for no-deposit or very low down payment insurance depends on a combination of driving behavior, financial stability, and coverage choices.

Clean Driving Record

A clean or mostly clean driving record is essential. Drivers without recent at-fault accidents, reckless driving violations, or serious infractions are viewed as lower risk. Even a single major violation can significantly increase deposit requirements.

Continuous Insurance Coverage

Continuous insurance coverage is another major factor. Insurers strongly prefer drivers who have maintained uninterrupted coverage for at least six to twelve months. Coverage lapses often trigger higher deposits or outright denials.

Coverage Selection

Coverage selection also matters. Drivers seeking liability-only coverage are far more likely to qualify for no-deposit plans than those requesting full coverage. Liability-only policies limit insurer exposure, making flexible billing more feasible.

Stable Personal Information

Stable personal information matters as well. Insurers look for consistency in address history, employment, and payment behavior. Frequent changes or prior nonpayment issues can reduce eligibility.

Credit Profile

Credit profile plays a supporting role. Drivers with fair to good credit are more likely to qualify for low-deposit plans, while those with poor credit often face higher upfront requirements.

When these factors align, drivers are in the strongest position to qualify for $20 down or zero-deposit insurance.

How Credit Score Impacts Down Payments

Insurance companies use credit-based insurance scores to predict payment behavior and claim frequency. Drivers with stronger credit are statistically more reliable, which allows insurers to offer lower deposits and more flexible billing.

Many insurers prefer scores in the mid-600s or higher when approving low-deposit plans. Drivers with scores above 700 often receive the best terms, including reduced deposits and lower monthly premiums.

Drivers with poor credit may still qualify, but deposits are often higher to offset perceived risk. Improving credit through on-time payments, debt reduction, and correcting credit report errors can significantly improve insurance affordability over time.

Vehicle Choice Plays a Major Role in Getting Cheap Coverage

The vehicle you drive has a major impact on deposit size and monthly premiums. Insurers evaluate how expensive a vehicle is to repair, how often it is involved in claims, and how likely it is to be stolen.

Older vehicles with lower market value are the easiest to insure with little money down. Four-door sedans, compact SUVs, and vehicles with four-cylinder engines typically qualify for lower deposits.

Low-performance vehicles designed for daily commuting present less risk than sports cars or luxury models. High-performance and high-value vehicles rarely qualify for no-deposit insurance, regardless of the driver’s record.

Mileage also matters. Vehicles driven fewer than 800 to 1,000 miles per month typically qualify for lower rates and deposits.

How Coverage Type Affects Deposit Size

Liability-only policies require the smallest deposits. Adding collision and comprehensive coverage increases insurer risk and deposit requirements.

Low-deposit full coverage may be available for older vehicles with modest value, high deductibles, strong credit, and low mileage. Financed or leased vehicles typically require higher upfront costs.

Liability-Only Coverage and Low Deposit Options

Liability-only coverage is the easiest way to qualify for no-deposit insurance. These policies meet legal requirements and cost less upfront.

However, they do not cover damage to your own vehicle. Drivers should carefully consider vehicle value and replacement ability before choosing liability-only coverage.

Full Coverage With No Money Down

Full coverage no-deposit insurance is rare, but low-deposit options may exist under favorable conditions. Older vehicles, high deductibles, strong credit, and low mileage improve eligibility. Financed vehicles usually require higher deposits.

Ways to Lower Both Your Deposit and Premium

Drivers can reduce costs by increasing deductibles, removing unnecessary add-ons, parking in secure locations, improving credit, and stacking discounts such as safe driver, senior, student, military, low-mileage, and automatic payment incentives.

Using these strategies together often results in dramatic savings.

Step-by-Step Checklist to Get Approved Faster

States Where No-Deposit Insurance Is More Common

Low-deposit and zero-deposit insurance structures are more common in states such as California, Florida, New York, Arizona, Georgia, Washington, and Oklahoma, though availability varies by insurer and profile.

Insurance Companies That Offer Low or No-Deposit Plans

Large national insurers are the most likely to offer low-deposit or no-deposit billing options because they operate with diversified risk pools across many states and driver profiles. This allows them to absorb short-term payment risk more effectively than smaller or regional carriers. Companies such as Progressive, Allstate, State Farm, Kemper, and SafeAuto often provide more flexible billing structures, including low upfront payments or installment-based plans.

Availability and terms depend heavily on individual eligibility, driving history, vehicle type, credit profile, and state regulations. Not every applicant will qualify, but these larger insurers tend to offer the widest range of deposit options, making them a strong starting point when shopping for no-money-down car insurance.

No Money Down Insurance for Young Drivers

Drivers under 25 face higher insurance costs due to increased accident risk. While zero-deposit insurance is rare, low-deposit options may exist when young drivers maintain clean records, drive older vehicles, choose liability-only coverage, and remain on a parent’s policy.

No Money Down Insurance for Seniors

Drivers aged 55 and older often qualify for the lowest deposits.

Seniors drive fewer miles, maintain long insurance histories, and pay bills reliably. Combined with discounts and older vehicles, they frequently receive the best low-deposit terms available.

Payment Options for No Money Down Policies

Most drivers choose monthly installment plans, though quarterly, semi-annual, and prepaid options may be available. Monthly billing offers flexibility but often increases total cost.

Accepted Payment Methods

Most insurers accept a wide range of payment methods, including debit cards, credit cards, bank transfers, online payment portals, and automatic withdrawals from checking or savings accounts. These options make it easier for drivers to manage monthly premiums without visiting an office or mailing payments.

Automatic payments are especially beneficial because they reduce the risk of missed due dates and policy cancellations. Many insurance companies also offer small discounts or fee reductions for enrolling in autopay, making it a simple way to improve payment reliability while potentially lowering overall costs.

Pros and Cons of No Money Down Auto Insurance

No money down auto insurance can be a practical solution for drivers who need coverage immediately but cannot afford a large upfront payment. One of the primary advantages is speed. These policies allow drivers to obtain coverage quickly, often the same day, helping drivers stay legally insured and avoid registration or licensing issues. Another important benefit is cash-flow flexibility. Instead of paying several hundred dollars upfront, drivers can spread costs across monthly payments, making insurance accessible during periods of temporary financial strain.

Despite these advantages, no-deposit insurance has clear drawbacks. Monthly premiums are almost always higher, which increases the total cost of coverage over time. What appears affordable at signup can become expensive over a six- or twelve-month policy term. Availability is also limited. Insurers may restrict these plans based on credit history, driving record, vehicle type, or prior coverage lapses. For this reason, no money down insurance works best as a short-term solution rather than a long-term cost-saving strategy.

Why No-Deposit Policies Often Cost More Long-Term

No-deposit auto insurance typically costs more over time because insurers shift financial risk into monthly pricing. When coverage begins with little or no upfront payment, insurers face a higher likelihood of early cancellation or missed payments. To offset this risk, companies increase monthly premiums and may apply installment-related fees.

Billing structure also affects long-term cost. Monthly installment plans generally cost more than semi-annual or prepaid policies due to administrative expenses and higher risk assumptions. Once a driver’s financial situation improves, switching to prepaid, semi-annual, or annual billing can significantly reduce overall insurance costs. No-deposit insurance solves an immediate need, but it is rarely the most economical option over the full policy term.

Improving Eligibility Over Time

Eligibility for no-money-down or low-deposit auto insurance can improve within six to twelve months through consistent behavior. Maintaining continuous insurance coverage is one of the most important factors. Avoiding lapses demonstrates reliability and often results in lower deposit requirements and more flexible billing options.

Improving credit also plays a major role. Paying bills on time, reducing outstanding balances, and correcting credit report errors can raise insurance-based credit scores. Driving behavior is equally important. Avoiding accidents, tickets, and violations gradually lowers risk classification. Reducing mileage and driving a lower-risk vehicle can further improve eligibility. Over time, these improvements often lead to lower deposits, lower premiums, and better payment flexibility.

If you want this applied to the entire article, say “do all sections,” and I’ll fix everything in one clean pass – no surprises, no formatting mistakes.

Why Online Comparison Is Essential

Every insurer calculates risk differently, which is why no money down and low-deposit pricing can vary so widely from one company to another. Insurance carriers use their own underwriting formulas, weighting factors such as credit history, driving record, vehicle type, mileage, location, and prior insurance coverage in different ways. As a result, a driver who is denied a low-deposit option by one insurer may qualify easily with another.

Comparing multiple quotes is the fastest and most effective way to identify the best combination of upfront deposit and affordable monthly payments. Looking at only one or two insurers often leads to overpaying, either through higher deposits or inflated premiums.

By reviewing several offers side by side, drivers can spot meaningful differences in billing structures, coverage options, deductibles, and total policy cost. This approach not only improves approval odds but also helps ensure that short-term affordability does not come at the expense of excessive long-term expense.

The Final Word on No Money Down Car Insurance

No money down car insurance is not free, but it is real. Used wisely, it allows drivers to stay insured during financial hardship while working toward better long-term options.

The smartest approach is to compare carefully, understand total cost, and treat low-deposit insurance as a stepping stone – not a permanent solution. Affordable coverage with minimal upfront cost is achievable with the right strategy. Compare no money down auto insurance plans in about 5 minutes and save serious money with direct rates.